.webp)

Climate Change’s Reckoning with the National Flood Insurance Program

It shouldn’t come as a surprise that the subsidized national flood insurance program is under increased strain due to impacts from climate change and the limited evolution of the program. The current solution is simply insufficient to address the growing problem and only getting worse.

The history of nationalized flood insurance

In 1968 Congress created the National Flood Insurance Program (NFIP) under Federal Emergency Management Agency (FEMA). The noble goal was, and still is today, to reduce the impact of flooding across the country by 1) providing flood insurance to property owners who live in communities that adopt and enforce floodplain management standards and 2) developing and implementing those standards. From 1968 to 2004 this program worked, it encouraged community action and more individuals to get insurance, voluntarily, and the program was able to pay out claims from the premiums it collected.

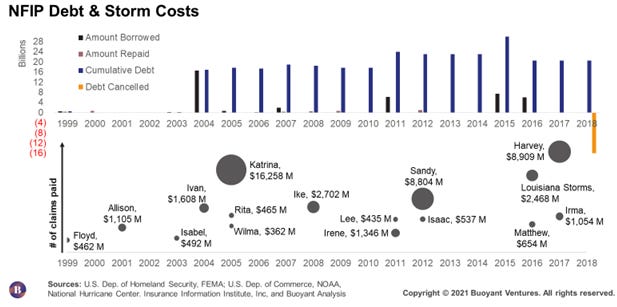

NFIP and Debt

However, the economics changed in the early 2000s. The number of policies in force had grown from about 2 to 2.5 million in the 80s and early 90s to 4.5 million as more communities were being impacted by storms and signing up for the program. In 2001 Tropical Storm Allison hit and resulted in over a billion dollars in payouts from the NFIP, this was followed by Hurricane Isabel ($492M) in 2003 and Hurricane Ivan ($1.6B) in 2004. NFIP could have likely recovered if there had been a few calm years, but in 2005 Hurricanes Katrina ($16.3B), Rita ($465M), and Wilma ($362M) all hit. Congress increased the NFIP’s borrowing limit from $1.5 billion to over $20 billion.

The following three decades have reinforced the message. The program’s borrowing limit was increased to over $30 billion in 2017 and today the NFIP has paid $5 billion in interest alone since 2005.

To be clear, none of the numbers mentioned above include government funding for disaster recovery, private insurance claims, uninsured losses, or the incalculable loss of life and livelihoods.

Change is coming

Today (October 1st) rates change for NFIP policyholders and will increase even more for new applicants. This is an overdue effort to update premium rates to be more closely aligned with a subject property’s risk. Climate change is calling for a reckoning. Updating the program is the right move but the impacts are hard to quantify with the rate analysis that FEMA and the NFIP have provided. Based on analysis from Delta Terra and risQ the update could increase premiums as much as 3x overnight. Their analyses also illustrate the economic and racial inequality that may only be exacerbated by these updates.

What’s next

This reckoning is long overdue. We must rethink how we better align insurance incentives when designing products, collecting better data to understand how our infrastructure is impacted, and considering the impacts on all citizens. This is a ripe area for digital technologies to aid in the truth-telling and pricing of climate change. We’re excited to share more of what we’ve been working on soon.

Related Posts

Subscribe to stay updated on news, insights, & invites to special events within our community.

We’re lighting the path forward for the ClimateTech industry—keep up with us along the journey.